All the facts and numbers of the footwear industry in 2021

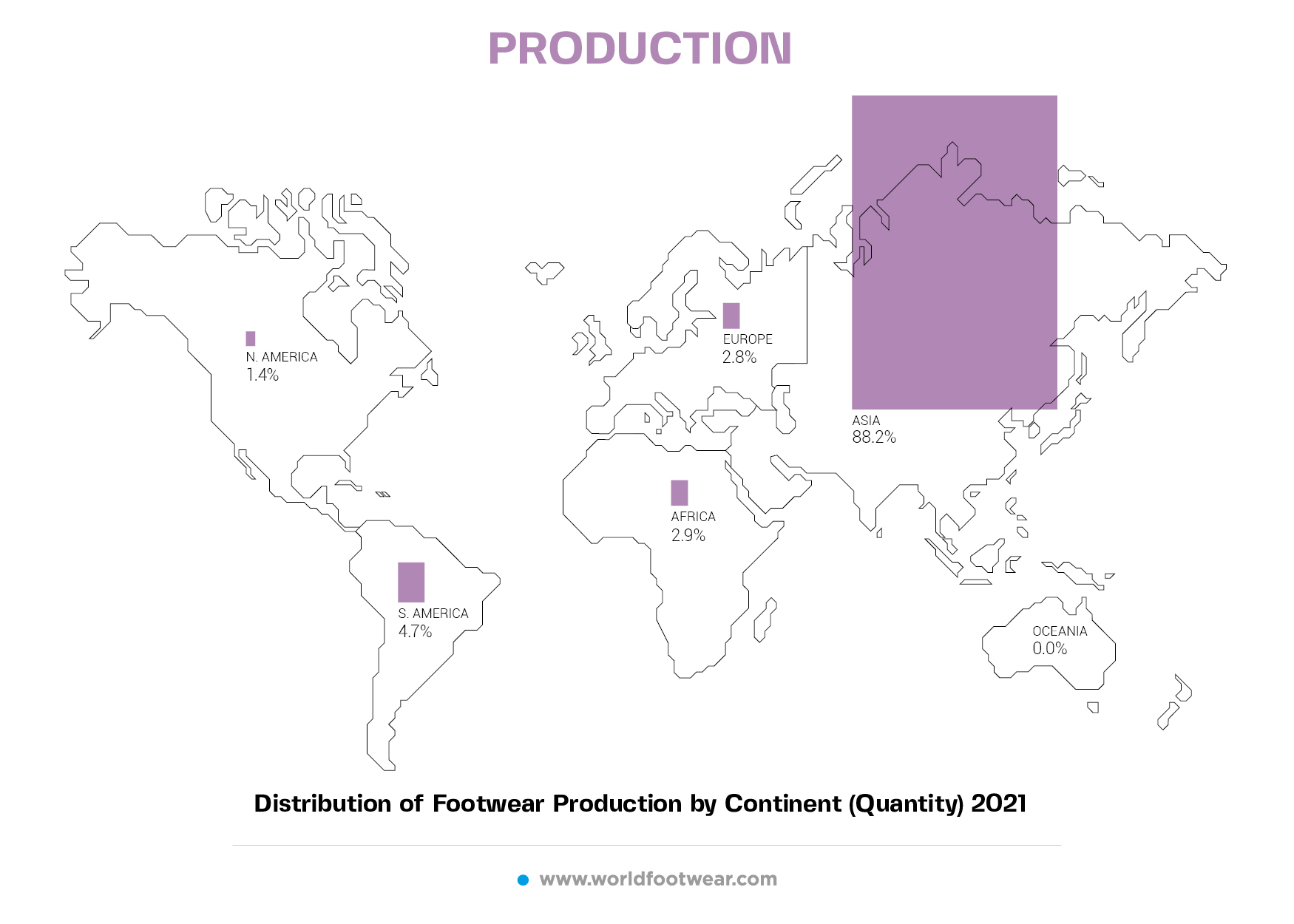

Last year, production and exports at global level grew by 8.6% and 7.4%, respectively. Worldwide footwear production exceeded the 22 billion pairs threshold but is still below pre-pandemic levels. In 2021, 13 billion pairs were exported worldwide, representing a partial recovery from the drop registered in 2020 but remaining below that of any other year in the last decade

Footwear production grows by 8.6% but is still below pre-pandemic levels

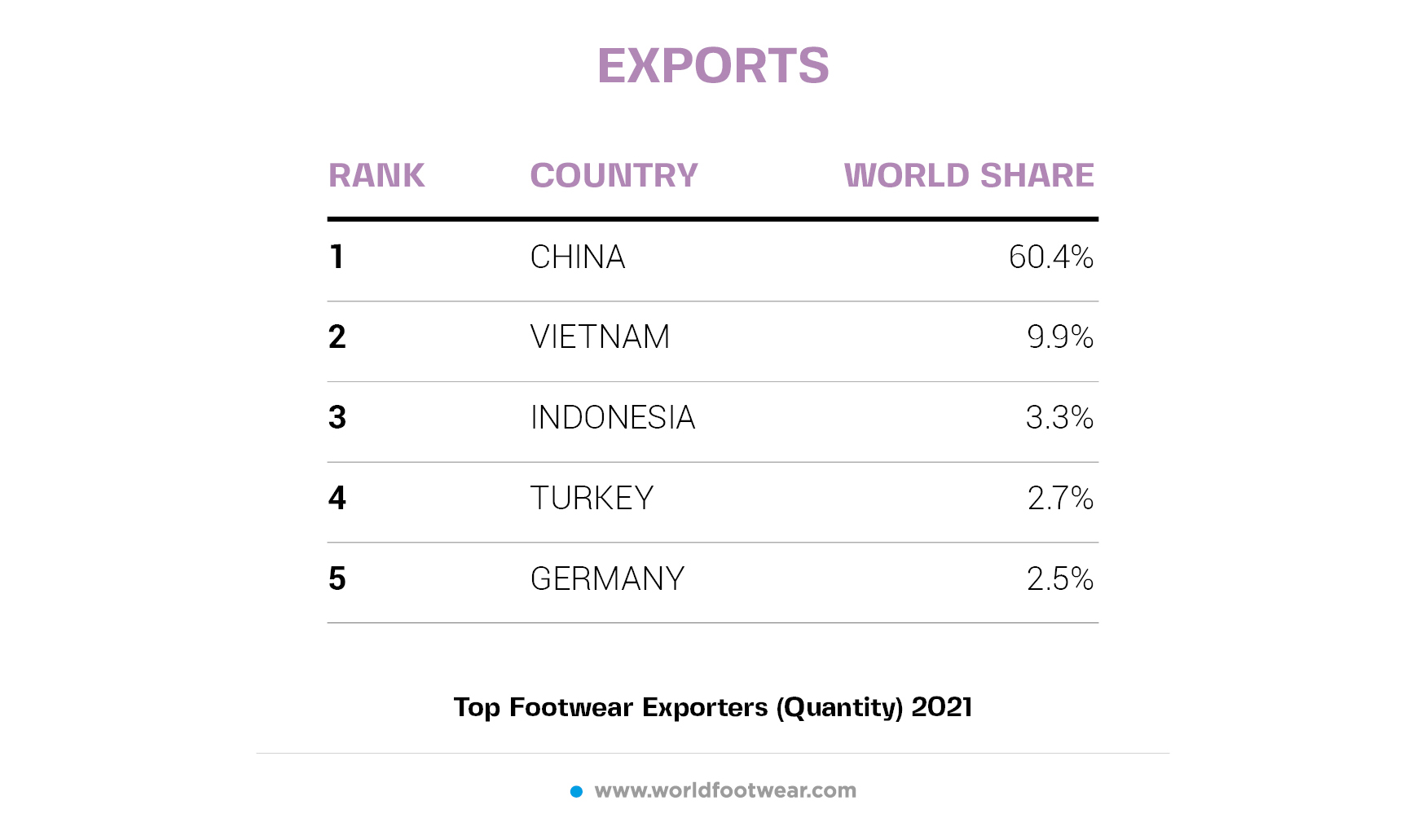

China is the world’s largest footwear producer (54.1%) but its share of the world production continues to slowly decrease in favour of other Asian countries, especially Vietnam. Over the last decade China has lost more than 6 percentage points of share.

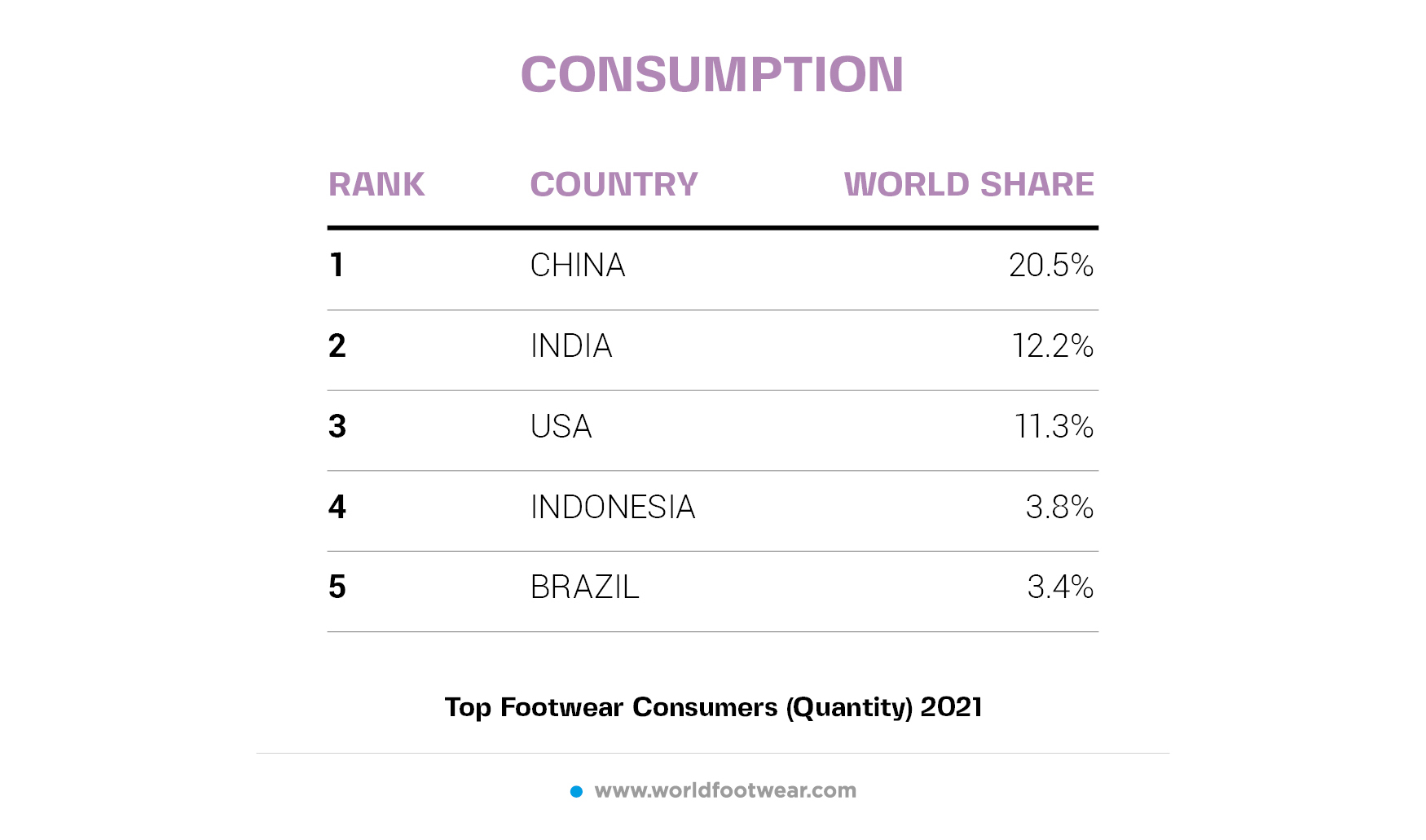

Asia accounts for more than half of global consumption

At country level, the distribution of consumption continues gradually to approach that of the population: China and India lead the top footwear consumer markets and together account for almost one third of world consumption. In third position, the United States, a major player of the industry, already fully recovered from the effects of COVID-19, with imports and consumption already standing at pre-pandemic levels. The European Union, when taken as one region, represents the fourth largest consumer market for footwear with 1 871 million pairs consumed in 2021.

Production aimed at external markets at the lowest level in a decade

Average worldwide export price exceeds 11 dollars for the first time

Data for this article was sourced from the World Footwear 2022 Yearbook

For more information about the World Footwear 2022 Yearbook click HERE

-

-

Footwear Consumer 2030

A study reflecting on the main global consumer trends and the key changes for the footwear industry.

-

World Footwear Public Calendar

Click here to subscribe an updated version of the calendar displaying the footwear trade shows.

-

-

Media Partners

Media Partners

-

SERMA

La Conceria

MPA Style

Shoe Intelligence